Oops! Something went wrong while submitting the form.

Team Building & Retreats tips

Updated on

April 24, 2026

Are Corporate Retreats Tax Deductible? A Planner's Honest Guide for 2026

You've been handed the retreat. The venue's almost booked, the agenda's coming together — and then someone in finance asks the question that makes your stomach drop: "Is any of this even tax deductible?"

Short answer: yes, most of it, when the retreat is built around a real business purpose and you've kept the receipts to prove it. The IRS doesn't blink at corporate retreats — it blinks at retreats that look like vacations with a "strategy session" sticker on the agenda. The difference is in how you scope, structure, and document the trip.

This guide walks through the rules the way a retreat planner thinks about them, not the way a tax textbook lists them. We've planned 2,000+ events — retreats are our specialty — and the deductibility question comes up on roughly every one of them. Here's what actually matters — and where you'll want a CPA to weigh in before you file.

⚠️ Disclaimer: This article is general information, not tax advice. Confirm your specific situation with a qualified CPA or tax attorney before claiming any deduction. IRS guidance changes — always cross-check the current rules at irs.gov.

- A corporate retreat is tax deductible when it passes three IRS tests: the expenses are ordinary and necessary for your business (IRC §162), the trip is primarily business rather than personal, and every cost is substantiated with proper documentation (Treas. Reg. §1.274-5).

- Travel and lodging for employees attending a primarily-business retreat are generally fully deductible. Meals are typically 50% deductible. Pure entertainment expenses are usually not deductible at all under the post-TCJA rules (IRC §274). Company-wide team-building events qualify for a special 100% deduction under §274(e)(4) when they're open to all employees and not skewed toward executives.

That's the headline. The rest of this guide is how to actually meet those tests in practice.

What Are the Three IRS Tests Every Retreat Has to Pass?

There's no single "retreat deduction" line in the tax code. Instead, three rules combine.

1. Ordinary and necessary

Under IRC §162(a), a business expense has to be both ordinary (common in your industry) and necessary (helpful and appropriate to the business). A two-day strategy and team-building retreat for a 50-person tech company easily clears this bar. A solo "founder's reflection week" at a five-star resort does not. (Background reading: the IRS's plain-English summary lives in Publication 463 — Travel, Gift, and Car Expenses.)

2. Primarily business

The IRS doesn't publish a magic percentage. Some advisory blogs cite "60% business activities" as a rule of thumb — that number isn't in the code, but it's a useful planner heuristic. What the IRS actually applies is a facts-and-circumstances test (Treas. Reg. §1.162-2(b)). For domestic trips, the question is whether business or personal motive primarily drives the trip. Day-count is the most defensible proxy: if 3 of 4 days are clearly business, the trip is primarily business.

3. Substantiated

Treas. Reg. §1.274-5 requires you to document five things for every expense: amount · time · place · business purpose · business relationship of any people involved. No documentation = no deduction, even if the expense was legitimate. This is where most disallowed deductions die.

If your retreat passes all three tests, the deductibility analysis becomes a line-item question — which is where most planners actually get tripped up.

Which Corporate Retreat Expenses Are Tax Deductible? (Line-Item Table)

This is the table we wish every CPA gave their clients before they planned the trip.

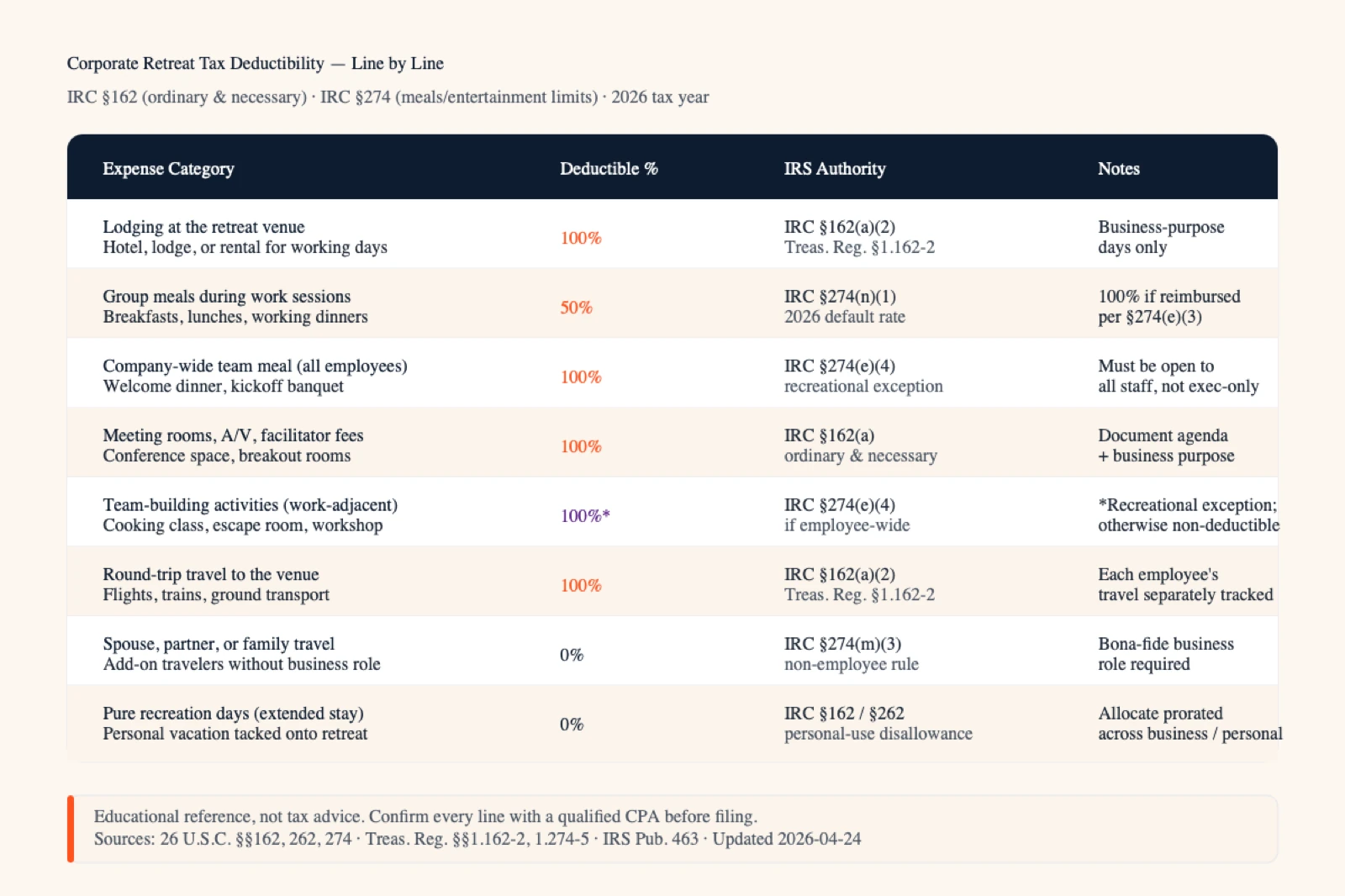

• Venue / meeting space — ✅ 100%. Notes: Conference rooms, breakout rooms, A/V rental — all ordinary business expenses

• Lodging (employees) — ✅ 100%. Notes: For nights related to the business portion of the trip

• Lodging (spouse / family) — ❌ Not deductible. Notes: Unless the spouse is also an employee with a bona fide business purpose for being there

• Round-trip travel (employees) — ✅ 100%. Notes: Flights, ground transport, mileage — when the trip is primarily business

• Meals during business sessions — ✅ 50%. Notes: Standard post-TCJA rule under §274(n)

• Company-wide social / team-building event — ✅ 100%. Notes: §274(e)(4) — must be primarily for non-highly-compensated employees, open to all

• Team-building activities tied to skill development — ✅ 50–100%. Notes: 100% if it qualifies as a company-wide event; otherwise treated like meals/entertainment depending on substance

• Pure entertainment (concert tickets, sporting events, spa) — ❌ Not deductible. Notes: TCJA eliminated the entertainment deduction in 2018

• Off-hours alcohol / parties unrelated to a business meeting — ❌ / Limited. Notes: Generally not deductible unless it falls under §274(e)(4)

• Branded swag / gifts (per recipient, per year) — ✅ Up to $25. Notes: §274(b)(1) caps the deduction at $25 per recipient annually; branded items under $4 may be excluded from the cap

• Conference / training fees — ✅ 100%. Notes: Ordinary business expense

• External speakers / facilitators — ✅ 100%. Notes: Ordinary business expense; strengthens the "primarily business" case

• Tangible items under $2,500 per invoice — ✅ 100% (deducted, not capitalized). Notes: De minimis safe harbor under Treas. Reg. §1.263(a)-1(f)

If a single line on this table changes the math on your retreat, that's exactly the kind of thing your CPA will want to see in writing before you book. Which is the next problem.

Which Corporate Retreat Expenses Are Not Tax Deductible?

The non-deductible list is shorter than the deductible one — but it's where most disallowed deductions actually originate. These are the line items that consistently get cut in audit:

• Spouse, partner, or family travel — disallowed under §274(m)(3) unless the spouse is also an employee with a documented business role for being there

• Pure entertainment — concert tickets, sporting events, golf rounds, spa treatments, theater outings disconnected from a business meeting. The TCJA eliminated this deduction entirely in 2018 (§274(a)(1)(A)); there's no "directly related" or "associated with" exception anymore

• Lavish or extravagant expenses — §162(a) requires expenses to be reasonable relative to the business benefit. A $40,000-per-night villa for a 3-person planning meeting fails this test even though lodging is a normally-deductible category

• Personal vacation days tacked onto the trip — if your team flies in two days early to ski, those two days (lodging, meals, activities) are personal and have to be backed out of the deduction

• Solo sightseeing, golf, spa, or recreation hours — even on an otherwise-business trip, the personal-time hours don't deduct, and they erode the "primarily business" defense for the rest of the trip

• Undocumented expenses of any size — substantiation is required for every business travel and meal expense regardless of dollar amount; the old "no receipt under $75" flexibility no longer applies to T&E

The cleanest defense against any of these getting reclassified is to plan for them honestly upfront — separate vendor invoices, separate billing for personal extensions, separate per diems for non-employee travelers.

How Meal and Entertainment Deductions Work at Corporate Retreats

Meals and entertainment used to share a tax category. The TCJA split them apart in 2018, and most retreats still get this wrong.

Meals (§274(n)(1)) — 50% deductible by default. Working breakfasts, working lunches, group dinners during the retreat — all 50% deductible as long as the meal isn't lavish, an employee is present, and the food is documented (vendor, date, attendees, business purpose). The temporary 100% restaurant-meal rate from 2021–2022 has expired; the default is back to 50%.

Entertainment (§274(a)(1)(A)) — 0% deductible. Concert tickets, sporting event tickets, golf greens fees, club dues, theater outings — none of these deduct, even if you discussed business during the activity. The line between "meal" and "entertainment" has gotten harder, not easier, since TCJA.

The separately-stated rule (IRS Notice 2018-76). If a meal is provided during an entertainment event (e.g., dinner at a baseball game), the meal can still be 50% deductible only if it's separately stated on the invoice. Bundled "all-in" pricing kills the meal deduction along with the entertainment portion. Tell your venue or vendor to itemize.

The §274(e)(4) exception — 100% for company-wide events. A welcome dinner, holiday party, or all-staff team-building activity that's open to all employees (and not skewed toward executives or owners) qualifies as employee recreation and is 100% deductible. This is the single most valuable carve-out for retreat planning — most well-structured retreats include at least one §274(e)(4) event by design.

How Much of a Corporate Retreat Has to Be Business Activity? (Agenda Test, Worked Example)

The agenda is the single most important piece of evidence in a deductibility audit. It's the first document the IRS asks for, and it's how you prove the trip was primarily business.

Here's what a defensible 3-day retreat agenda looks like — built around the structure that holds up under scrutiny.

Day 1 — Travel and arrival

• 8:00 AM – 6:00 PM: Travel

• 6:30 PM: Welcome dinner with all-hands roadmap presentation by CEO (business meal, 50% deductible)

That's roughly 11 hours of documented business activity across 3 days, with structured sessions, a deliverable trail (workshop outputs, OKR documents, action items), and a clear external speaker. A schedule like this defends itself.

A schedule that doesn't defend itself: a 4-day "strategy retreat" with one 90-minute meeting and three days of ski-resort activities. That's not a retreat — that's a vacation with a calendar invite.

What Documentation Do You Need for a Corporate Retreat Tax Deduction?

If the IRS examines your retreat deduction, this is what they'll request — and what you should already have on file before the trip ends.

• ✅ Final written agenda with timestamps for each session and named facilitators

• ✅ Attendee list with employee names, roles, and (if non-employees attended) the business reason for their presence

• ✅ Stated business objectives for the retreat — written down before the trip, not reverse-engineered after

• ✅ All receipts — venue, lodging, F&B, transport, activities — even items under $75 (the IRS no longer has a flexible "no-receipt" threshold for travel)

• ✅ Expense report filed under your accountable plan (Treas. Reg. §1.62-2) so reimbursements stay out of employees' income

• ✅ Separate line items for any spouse or family expenses (which you should plan for the attendees to cover personally)

• ✅ Receipts and itineraries kept for 3 years minimum (the standard IRS lookback for examined returns)

Your retreat planner should be helping you build this record in real time, not asking you to reconstruct it three months later. If you want a head start, our corporate retreat planning checklist covers the documentation a CPA will want to see, alongside the rest of the pre-retreat prep.

Company Outings vs. Corporate Retreats: Why the Tax Rules Differ

Both involve employees, food, and activities — but the tax code treats them very differently, and the distinction shows up on the return.

A company outing is an employee-recreation event: holiday party, summer picnic, all-staff happy hour, single-day team-building activity. These are deductible at 100% under §274(e)(4) because the IRS treats them as a fringe benefit primarily for the rank-and-file workforce. The catch: they have to be open to all employees and not skewed toward executives or highly-compensated employees. Exec-only "leadership outings" drop back to 50% (for any meal portion) or 0% (for any entertainment portion).

A corporate retreat is a business event: strategic planning, leadership offsite, sales kickoff, product launch, all-hands. The deduction is driven by the agenda and IRC §162's ordinary-and-necessary test, not by §274(e)(4). Retreat expenses split across the line items above — 100% lodging and travel, 50% working meals, 100% meeting space, 0% pure entertainment.

Many real retreats include outing-style components — a welcome dinner, a group activity, a closing celebration. The tax treatment splits: the welcome dinner can ride §274(e)(4) at 100% if it's open to all attendees; the strategy workshop is 100% deductible business; the working lunch is 50%. Your CPA needs the agenda to allocate correctly.

The keyword distinction matters for finance teams: "is a company outing tax deductible" is asking about §274(e)(4); "is team building tax deductible" depends on whether the activity qualifies under §274(e)(4) or gets caught by §274(a)(1)(A); "are corporate retreats tax deductible" is asking about §162 + §274 combined.

Sole Proprietor vs. C-Corp vs. S-Corp — Why It Matters

How you're structured changes both what you can deduct and where the deduction lands.

• C-corporation: Deducts retreat expenses on the corporate return (Form 1120). Shareholder-employees are treated like other employees — their travel, lodging, and 50% of meals are deductible to the corporation. Most of the discussion in this guide assumes a C-corp or S-corp structure.

• S-corporation: Same general rules as a C-corp at the entity level, but deductions flow through to shareholders' personal returns. Owner-employees still need a documented business purpose; the IRS scrutinizes S-corp retreats with high owner-personal benefit harder than C-corp ones.

• Sole proprietor: Deducts on Schedule C. The "team retreat" framing is harder to apply if you have no employees. Solo working trips are evaluated under standard business-travel rules (IRS Topic 511 — Business Travel Expenses) and have to clear the "primarily business" bar without the cover of a group event. Many sole proprietors over-claim here; CPAs frequently disallow the leisure portion in audit.

If you're a sole proprietor planning a "retreat" with one or two contractors, talk to your CPA before booking — the substance test is stricter than people expect.

A Note on California (and Other High-Audit States)

State income tax rules generally follow federal deductibility, but California, New York, and a few other high-audit states sometimes apply tighter substantiation in practice — especially around meals, entertainment, and out-of-state retreats. California's Franchise Tax Board has historically scrutinized retreat deductions more closely than federal examiners do, and the state's own franchise tax rules don't always conform to federal treatment.

If your company is California-based and your retreat is held out of state, two things to watch:

1. The "primarily business" test gets more attention when the destination is a known leisure spot (Hawaii, Tahoe, Wine Country)

2. Your CPA may want stronger contemporaneous documentation than what passes federally

Picking a venue type that signals "working offsite" rather than "luxury escape" is the cheapest defensive move you can make — conference-equipped lodges, dedicated retreat venues, and working hotels all read as business settings in a way a beachfront resort doesn't. This isn't a reason to host the retreat at the office; it's a reason to make the agenda and documentation airtight regardless of where you go.

Common Mistakes That Trigger IRS Scrutiny

These are the patterns that consistently move a retreat deduction from "routine" to "examined" — drawn from CPA-side audit experience and IRS examination guides.

1. Vague or post-hoc agenda — Can't substantiate "primarily business" — looks reverse-engineered after the fact. How to avoid it: Lock a documented agenda with named facilitators before the trip; preserve the original version with timestamps

2. Spouse / family on the company tab — §274(m)(3) violation — classic disallowance trigger; jumps out in any audit sample. How to avoid it: Bill personal travelers separately at booking; if a spouse attends a session, document the bona fide business role

3. Resort destination + thin business hours — Personal-use disallowance under §162; the "destination test" looks at substance vs. setting. How to avoid it: Hit the majority-of-waking-hours benchmark with structured sessions; keep workshop outputs as proof

4. Missing or aggregated receipts — §274(d) substantiation failure — every expense needs amount, date, place, business purpose, attendees. How to avoid it: Collect every receipt, no matter how small; never reconstruct after the fact (auditors can tell)

5. Pure entertainment relabeled as "team building" — §274(a)(1)(A) — entertainment is 0% deductible post-TCJA, regardless of the label on the invoice. How to avoid it: Keep entertainment to §274(e)(4)-qualifying events (open to all employees, not exec-skewed); separately state any meals provided during entertainment

If your retreat has even two of these patterns, the deduction is fragile. Three or more, and a careful CPA will tell you to either restructure the trip or plan to defend it. None of these are hard to avoid — they're just hard to fix retroactively.

What Counts as a Corporate Retreat in the Eyes of the IRS?

A corporate retreat is an organized, multi-day off-site gathering of employees structured around a documented business purpose — strategic planning, leadership development, team-building tied to skill development, sales kickoffs, all-hands meetings, product launches, or quarterly OKR setting. The IRS doesn't define "retreat" as a separate category in the tax code; instead, it evaluates the trip under the same rules that govern any business travel and meals (IRC §162, §274, Treas. Reg. §1.162-2). What turns a vacation into a retreat — in tax terms — is the substance of the agenda, not the label on the calendar invite. A two-day strategy offsite with documented sessions, named facilitators, and recorded outcomes is a retreat. A four-day "team trip" with one happy hour and three days of skiing is a vacation. The line is drawn by the agenda, the documentation, and the proportion of the trip given over to genuine business activity — and that's the line the IRS examines first.

FAQ

A company retreat is tax-deductible when it passes three IRS tests: the expenses are ordinary and necessary for your business (IRC §162), the trip is primarily business rather than personal (Treas. Reg. §1.162-2), and every cost is properly substantiated with contemporaneous documentation (Treas. Reg. §1.274-5). For a retreat that meets these tests, employee travel and lodging are generally 100% deductible, meals during business sessions are 50% deductible under §274(n), and qualified team-building activities tied to a company-wide event can be 100% deductible under §274(e)(4). Pure entertainment expenses — concert tickets, sporting events, spa days disconnected from business sessions — are generally not deductible post-TCJA. Spouse and family travel costs are not deductible unless the spouse is also an employee with a bona fide business purpose for attending.

A company retreat is an organized off-site gathering of employees structured around a clear business purpose — strategic planning, team-building tied to skill development, leadership offsites, training, sales kickoffs, all-hands meetings, or product launches. To qualify for a tax deduction, the agenda has to demonstrate the business purpose with documented sessions, named facilitators, and recorded outcomes — not just a label on the calendar invite. The IRS evaluates retreats on substance, not branding: a two-day workshop with structured agenda blocks, an external facilitator, and written deliverables is a retreat in tax terms. A loosely-structured "team trip" with one all-hands meeting and three days of unstructured time is much harder to defend. The agenda is your single most important piece of evidence — it's the first document the IRS asks for in an examination, and it's how you prove the trip was primarily business.

The $2,500 figure refers to the IRS de minimis safe harbor under Treas. Reg. §1.263(a)-1(f), which lets businesses immediately deduct (rather than capitalize and depreciate) tangible property purchases of $2,500 or less per invoice or per item. For a corporate retreat, this matters when you buy things like A/V equipment, branded swag, presentation supplies, or any tangible asset for the event — purchases at or below $2,500 per invoice can be expensed in the year incurred, while purchases above $2,500 generally have to be capitalized and depreciated over their useful life. The election applies on a per-invoice basis, not per total spend, so structuring vendor invoices below the threshold (when legitimate) is a common planning move. For taxpayers with applicable financial statements, the threshold rises to $5,000.

Often yes. Company-wide team-building events that are primarily for non-highly-compensated employees and open to all qualify for a 100% deduction under §274(e)(4) — this is a narrow but valuable exception to the post-TCJA entertainment disallowance. Smaller team-building activities tied to a business retreat are typically deductible as part of the broader business event, with meals at 50% and any pure-entertainment portions disallowed.

Generally no. Wellness retreats — yoga, meditation, spa, personal-development weekends — fail the "ordinary and necessary" business test for most companies because the IRS treats the benefit as primarily personal to the attendee. There are narrow exceptions where wellness sessions are part of a documented employee health program, but stand-alone wellness trips are usually not deductible.

Harder than for corporations. Sole proprietors deduct on Schedule C and have to clear the "primarily business" test on their own — with no employees to anchor the team-building justification. Solo working retreats are evaluated under standard business-travel rules (IRS Topic 511); the leisure portion is frequently disallowed in audit. Talk to your CPA before assuming a deduction.

Yes, but the rules are stricter. Foreign business travel under §274(c) and

How to Plan a Tax-Deductible Corporate Retreat

A defensible retreat deduction comes from four planning moves, all made before day one:

1. Lock the agenda first. Build the day-by-day schedule before you sign the venue contract. If you can't fill the majority of waking hours with documented business activities, the deduction is at risk — restructure the trip or shorten it.

2. Pick a venue that signals "working offsite," not "luxury escape." Conference-equipped lodges, working hotels, and dedicated retreat venues hold up better than five-star resorts in beach destinations. The §162 reasonableness test is implicit in the venue choice.

3. Set up the documentation system before day one. Decide who's collecting receipts, who's writing the outcomes summary, who's tracking attendees and signed agendas. The cheapest hour you'll spend on this retreat is the one you spend setting up the paper trail in advance.

4. Separate the personal stuff at booking, not after. If anyone is bringing a spouse, extending for vacation, or upgrading their room — bill those costs to them directly. Mixing them into the company invoice creates work for your CPA and risk for the deduction.

If budget is the bottleneck driving these calls, our breakdown of what corporate retreats actually cost in 2026 shows where the deductible-vs-non-deductible split usually lands across venue, F&B, and activity line items.

Most companies underestimate how much of the deductibility question is decided in the planning phase, not the filing phase. By the time you're handing receipts to your CPA, the structural decisions are already made. Companies like Netflix, Brex, and L'Oréal use exactly this kind of documentation pattern on the retreats we plan with them — built into the agenda before day one, not reconstructed at year-end.

This is the kind of detail a dedicated retreat planning partner handles as a default — agenda built around defensible business blocks, vendor receipts collected and organized, attendee records kept clean, and a structured outcomes summary at the end. If you'd rather spend your time on the team experience than the audit trail, that's the work to delegate.

Thomas Mazimann, a French entrepreneur and former international kayaking athlete, transitioned from sports to tech after moving to the U.S. He co-founded TeamOut, revolutionizing team gatherings.